If you’ve been injured on the job and are receiving workers’ compensation benefits, you may be wondering, “Is workers comp taxable?” The good news is that, in most situations, workers’ compensation benefits are not subject to federal income tax. However, there are a few important exceptions that every injured worker should understand, especially if they also receive Social Security Disability Insurance (SSDI), retirement benefits, or other taxable income.

Knowing how workers’ compensation is taxed can help you avoid confusion during tax season and better understand your financial situation while recovering from a workplace injury. In this guide, we’ll explain when workers’ compensation is tax-free, when it can indirectly affect your taxes, how it interacts with Social Security benefits, and what records you should keep for your tax return.

Whether you’re receiving weekly disability payments or negotiating a lump-sum settlement, this article covers everything you need to know in simple, easy-to-understand language.

Quick Answer

No. Workers’ compensation benefits are generally not taxable at the federal level.

According to the Internal Revenue Service (IRS), benefits paid under a state’s workers’ compensation law because of a work-related injury or illness are usually excluded from gross income. That means most people do not pay federal income tax on these benefits.

However, there are exceptions. Your overall tax situation can become more complicated if:

- You also receive Social Security Disability Insurance (SSDI) benefits.

- Your SSDI benefits are reduced because of a workers’ compensation offset.

- You receive other taxable income, such as wages, pension payments, or investment income.

- Part of a legal settlement includes taxable payments that are separate from workers’ compensation benefits.

Understanding these situations can help you avoid unexpected tax issues.

What Is Workers’ Compensation?

Workers’ compensation is a state-regulated insurance program that provides benefits to employees who suffer a work-related injury or illness. Nearly every state requires employers to carry workers’ compensation insurance or participate in an approved self-insurance program.

Workers’ compensation is designed to protect both employees and employers. Instead of filing a lawsuit against an employer in most situations, injured workers can receive benefits regardless of who caused the workplace accident.

Depending on your state’s laws, workers’ compensation benefits may include:

- Medical treatment

- Hospital and emergency care

- Prescription medications

- Physical therapy and rehabilitation

- Temporary disability benefits

- Permanent disability benefits

- Vocational rehabilitation

- Mileage reimbursement for medical travel (where applicable)

- Death benefits for eligible surviving family members

These benefits help injured workers recover financially while they are unable to perform their regular job duties.

Official Source: Internal Revenue Service – Publication 525, Taxable and Nontaxable Income

How Does Workers’ Compensation Work?

Although each state’s workers’ compensation system is different, the general process is similar across the United States.

Here’s how it typically works:

- A workplace injury or illness occurs.

- The employee reports the injury to the employer within the required timeframe.

- Medical treatment is provided according to state workers’ compensation rules.

- A workers’ compensation claim is filed.

- The insurance carrier reviews the claim.

- Benefits are paid if the claim is approved.

Benefits may continue until the employee returns to work, reaches maximum medical improvement, or receives a settlement, depending on the circumstances.

Because workers’ compensation replaces lost wages and covers medical costs related to workplace injuries, Congress generally excluded these benefits from federal income taxation.

Types of Workers’ Compensation Benefits

Not all workers’ compensation benefits serve the same purpose. Understanding the different types can help explain why most of them are tax-free.

Medical Benefits

Medical benefits typically cover treatment related to your workplace injury or illness, including:

- Doctor visits

- Surgery

- Hospital care

- Diagnostic testing

- Prescription medications

- Physical therapy

- Medical equipment

Since these payments reimburse healthcare costs rather than provide taxable income, they are generally not taxable.

Temporary Total Disability (TTD)

If your injury prevents you from working for a limited period, you may receive temporary disability payments that replace part of your lost wages while you recover.

Although these payments replace income, they are generally not considered taxable wages under federal law.

Temporary Partial Disability (TPD)

Some injured employees can return to work with restrictions and earn less than they did before the injury.

Temporary partial disability benefits may compensate for part of the difference between your previous earnings and your reduced wages.

These benefits are generally treated the same as other workers’ compensation payments for federal tax purposes.

Permanent Partial Disability (PPD)

If a workplace injury causes permanent impairment but you can still work in some capacity, you may qualify for permanent partial disability benefits.

Examples include:

- Permanent loss of hearing

- Partial loss of vision

- Loss of use of a hand, arm, foot, or leg

- Other permanent physical impairments

These benefits are generally tax-free when paid under a state’s workers’ compensation law.

Permanent Total Disability (PTD)

Some workplace injuries permanently prevent an employee from returning to any type of substantial work.

In these situations, workers’ compensation may provide ongoing disability payments or a negotiated settlement.

These payments are generally excluded from federal taxable income.

Vocational Rehabilitation Benefits

If your injury prevents you from returning to your previous occupation, workers’ compensation may provide vocational rehabilitation services, such as:

- Job training

- Career counseling

- Educational programs

- Resume assistance

- Job placement services

These services are intended to help injured workers return to suitable employment and are generally not taxable.

Death Benefits

If a worker dies because of a job-related injury or illness, eligible dependents may receive workers’ compensation death benefits.

These payments often help surviving family members cover:

- Funeral expenses

- Lost financial support

- Ongoing survivor benefits

Federal tax law generally excludes these workers’ compensation death benefits from taxable income.

Is Workers Comp Taxable?

For most injured workers, the answer is simple:

No. Workers’ compensation benefits are generally not taxable under federal law.

The IRS specifically states that amounts you receive as workers’ compensation for an occupational sickness or injury under a workers’ compensation act or similar statute are excluded from your taxable income.

This means you generally do not report workers’ compensation benefits as income on your federal tax return.

Examples of benefits that are usually not taxable include:

- Weekly workers’ compensation checks

- Temporary disability benefits

- Permanent disability payments

- Medical reimbursements

- Rehabilitation benefits

- Lump-sum settlements that replace workers’ compensation benefits

- Survivor benefits paid under workers’ compensation laws

For many injured workers, this tax-free treatment provides important financial relief while recovering from an injury.

Official Source: Internal Revenue Service – Publication 525, Taxable and Nontaxable Income

Why Doesn’t the IRS Tax Workers’ Compensation?

Many people assume that because workers’ compensation replaces lost wages, it should be taxed like a paycheck. However, federal tax law treats these benefits differently.

Workers’ compensation is intended to compensate employees for a work-related injury or illness rather than reward them for performing work. Since the payments are part of a statutory insurance system designed to protect injured workers, Congress excluded qualifying benefits from taxable income.

This tax-free treatment helps ensure that injured employees can focus on recovery without losing part of their benefits to federal income taxes.

Even though the benefits replace a portion of lost earnings, they are not considered regular wages for federal income tax purposes.

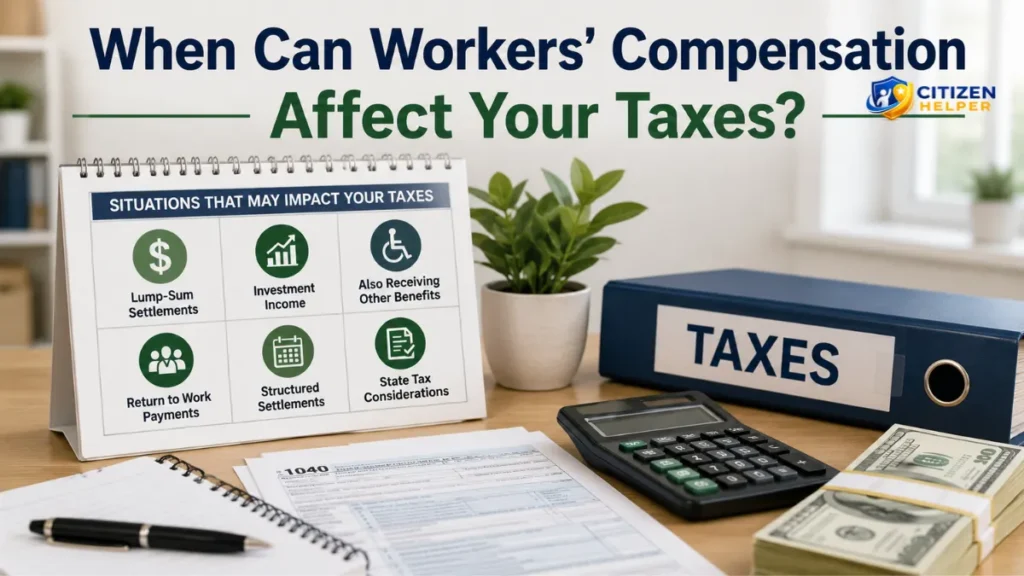

When Can Workers’ Compensation Affect Your Taxes?

Although workers’ compensation benefits are generally tax-free, there are situations where they can indirectly affect your overall tax picture. In most of these cases, it is not the workers’ compensation benefit itself that becomes taxable. Instead, receiving multiple types of benefits can change how other income is treated under federal tax law.

Here are the most common situations to understand.

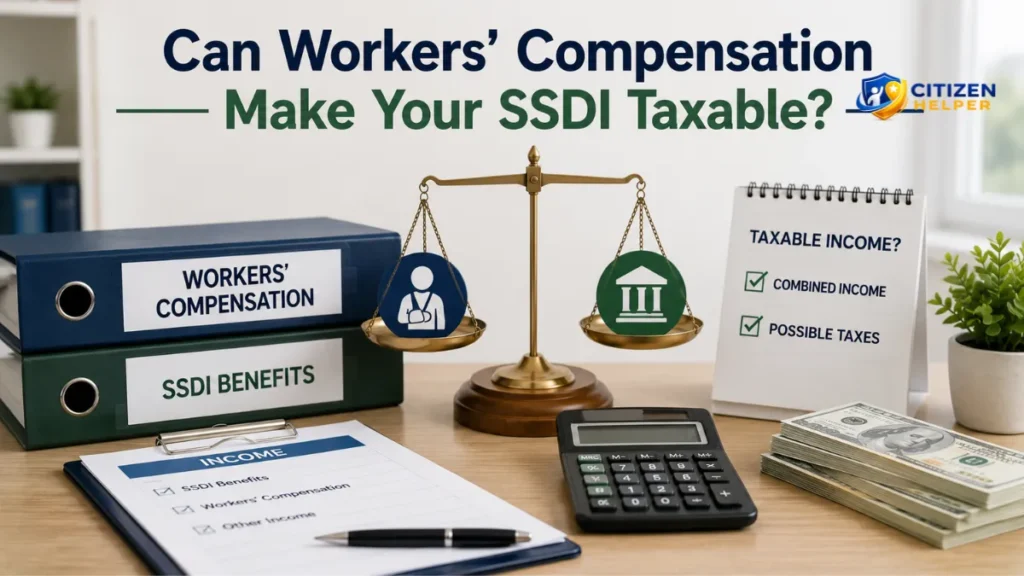

Workers’ Compensation and SSDI Benefits

One of the most important exceptions involves Social Security Disability Insurance (SSDI).

If you qualify for both workers’ compensation and SSDI, federal law limits the total amount of disability benefits you can receive.

In many cases, the combined total of your workers’ compensation and SSDI benefits cannot exceed 80% of your average current earnings before you became disabled. If your combined benefits exceed this limit, the Social Security Administration (SSA) may reduce your SSDI payments. This reduction is known as the workers’ compensation offset.

It’s important to understand that:

- Your workers’ compensation benefits generally remain tax-free.

- The offset reduces your SSDI payment rather than your workers’ compensation payment.

- Depending on your total income, part of your SSDI benefits may still be taxable under IRS rules.

This is one of the main reasons some people become confused about whether workers’ compensation is taxable.

Can Workers’ Compensation Make Your SSDI Taxable?

Not directly.

Workers’ compensation itself does not become taxable simply because you receive SSDI.

However, if the IRS treats part of your reduced SSDI benefit as Social Security income for tax purposes, you could owe tax on a portion of your SSDI depending on your combined income.

Whether SSDI is taxable depends on several factors, including:

- Filing status

- Combined income

- Other taxable income

- Tax-exempt interest

- Half of your Social Security benefits

Because every taxpayer’s situation is different, the amount of taxable SSDI can vary.

What About SSI?

Many people confuse Supplemental Security Income (SSI) with SSDI, but they are different programs.

SSI is a needs-based benefit, while SSDI is based on your work history and payroll tax contributions.

Workers’ compensation generally does not receive the same type of offset treatment with SSI that applies to SSDI. However, receiving workers’ compensation could affect SSI eligibility or payment amounts because SSI has strict income and resource rules.

If you receive SSI, report changes in income or benefits to the Social Security Administration as required.

Are Lump-Sum Workers’ Compensation Settlements Taxable?

Many workers’ compensation claims end with a lump-sum settlement rather than ongoing weekly checks.

In most situations, a lump-sum workers’ compensation settlement is not taxable if it represents benefits payable under your state’s workers’ compensation law.

For example, a settlement may include compensation for:

- Future wage replacement

- Permanent disability

- Future medical care

- Vocational rehabilitation

- Other workers’ compensation benefits

These amounts are generally excluded from federal taxable income.

However, every settlement agreement is unique.

Some settlements may include payments that are not workers’ compensation benefits, such as:

- Interest paid on delayed benefits

- Punitive damages in certain legal cases

- Employment-related payments outside the workers’ compensation claim

These types of payments may have different tax treatment.

If your settlement includes multiple types of compensation, consider asking a qualified tax professional to review the agreement.

Are Attorney Fees Taxable?

Many injured workers hire an attorney to help with their workers’ compensation claim.

In general, attorney fees paid from a workers’ compensation award do not change the tax-free nature of the workers’ compensation benefits themselves.

However, if your legal case involves additional claims outside the workers’ compensation system, different tax rules may apply to those payments.

Do You Receive a W-2 or 1099 for Workers’ Compensation?

Usually, no.

Because workers’ compensation benefits are generally not taxable income, recipients typically do not receive:

- Form W-2

- Form 1099-NEC

- Form 1099-MISC

Instead, your workers’ compensation insurance carrier keeps records of the payments without reporting them as taxable wages.

If you receive taxable wages after returning to work, or receive another taxable payment unrelated to workers’ compensation, you may receive the appropriate tax forms for those amounts.

Does Workers’ Compensation Affect Your Tax Return?

For most taxpayers, workers’ compensation benefits are not reported as taxable income on a federal income tax return.

However, your overall tax return may become more complicated if you also receive:

- SSDI benefits

- Pension income

- Retirement distributions

- Investment income

- Self-employment income

- Wages from a new or part-time job

Although workers’ compensation itself usually stays tax-free, these other income sources may affect your overall tax liability.

Keeping organized records throughout the year can make filing your tax return much easier.

Is Workers’ Compensation Taxable by Your State?

Federal law generally excludes workers’ compensation benefits from taxable income. Many states follow the same approach, but state tax laws are not identical.

Some states have different rules regarding disability income, retirement benefits, or related payments.

Because state tax laws can change over time, it’s important to verify the latest guidance from your state’s tax authority.

Check your state’s department of revenue or official tax agency for the most current rules.

Avoid relying on outdated online information or tax advice that isn’t specific to your state.

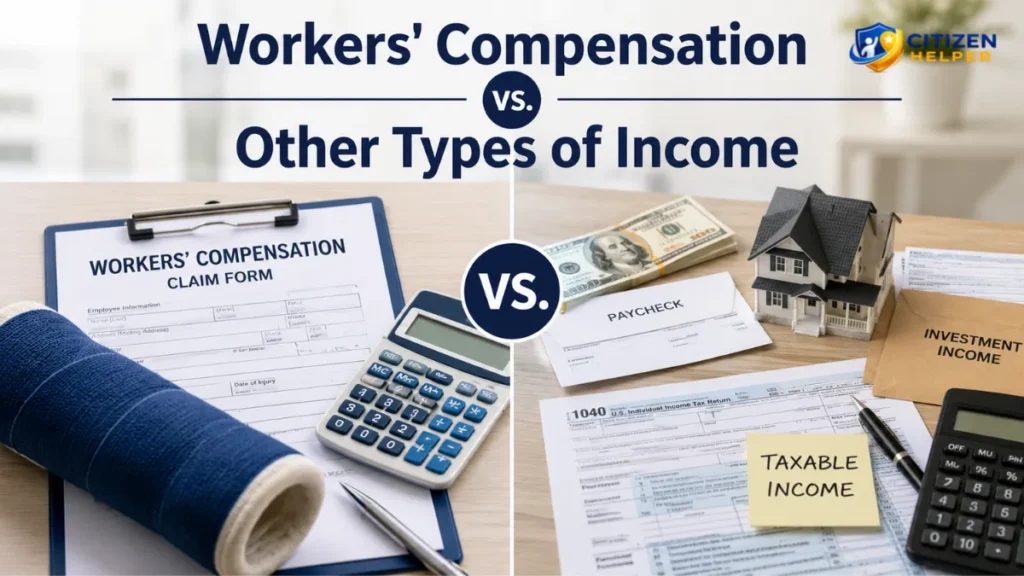

Workers’ Compensation vs. Other Types of Income

Understanding how workers’ compensation compares with other common benefits can help clear up tax confusion.

| Type of Income | Usually Taxable? | Notes |

| Workers’ compensation | Generally No | Usually excluded from federal income tax. |

| SSDI | Sometimes | May be taxable depending on your combined income. |

| SSI | Generally No | Needs-based benefit, not subject to federal income tax. |

| Social Security retirement | Sometimes | May be partially taxable based on total income. |

| Regular wages | Yes | Subject to federal income tax and payroll taxes. |

| Pension income | Often | Taxability depends on the type of pension and your circumstances. |

| Unemployment compensation | Generally Yes | Usually taxable for federal income tax purposes. |

Real-Life Examples

The following examples illustrate how workers’ compensation benefits are generally treated for tax purposes.

Example 1: Temporary Workplace Injury

Maria injures her shoulder while working in a warehouse and receives workers’ compensation benefits for four months while recovering.

Because her payments are made under her state’s workers’ compensation law, she generally does not pay federal income tax on those benefits.

Example 2: Receiving Workers’ Compensation and SSDI

James receives workers’ compensation after a serious workplace accident. He also qualifies for SSDI.

Because his combined disability benefits exceed the federal limit, the SSA reduces his SSDI payment through a workers’ compensation offset.

His workers’ compensation benefits generally remain tax-free, although his SSDI may have separate tax considerations.

Example 3: Lump-Sum Settlement

Angela settles her workers’ compensation claim for a lump-sum payment that replaces future disability benefits.

As long as the settlement represents workers’ compensation benefits under state law, the payment is generally not subject to federal income tax.

Example 4: Returning to Work

After recovering from a back injury, David returns to work and begins earning regular wages again.

His previous workers’ compensation benefits generally remain tax-free, but his new wages are taxable like any other employment income.

Common Tax Mistakes to Avoid

Although workers’ compensation benefits are generally tax-free, misunderstandings about the rules can lead to mistakes when filing your tax return. Here are some common errors to avoid.

Assuming All Disability Benefits Are Tax-Free

Many people think every disability-related payment receives the same tax treatment. In reality, workers’ compensation, SSDI, SSI, private disability insurance, and employer-provided disability benefits may each have different tax rules.

Before filing your return, make sure you understand which benefits you received and how each one is treated for tax purposes.

Reporting Workers’ Compensation as Taxable Income

Some taxpayers mistakenly include workers’ compensation payments as wages or other income on their federal tax return.

In most cases, workers’ compensation benefits paid under a state’s workers’ compensation law should not be reported as taxable income.

Ignoring an SSDI Offset

If you receive both workers’ compensation and SSDI, the Social Security Administration may reduce your SSDI benefits through a workers’ compensation offset.

Failing to understand how this offset affects your overall tax situation can lead to confusion when preparing your return.

Misunderstanding Settlement Agreements

Not every payment included in a legal settlement is automatically tax-free.

While workers’ compensation benefits are generally excluded from federal income tax, other payments included in a settlement—such as interest or compensation unrelated to the workers’ compensation claim—may have different tax treatment.

Carefully review your settlement documents if you receive a lump-sum payment.

Throwing Away Important Records

Even though workers’ compensation is generally tax-free, you should keep copies of:

- Benefit statements

- Settlement agreements

- Medical records related to the claim

- Letters from the workers’ compensation insurance carrier

- Social Security notices if you receive SSDI

Keeping these records can help answer questions if they arise later.

Tips for Filing Taxes While Receiving Workers’ Compensation

Tax season is usually straightforward for workers receiving only workers’ compensation benefits. Still, a few simple steps can help ensure an accurate tax return.

Consider these best practices:

- Keep detailed records of all benefits you receive.

- Separate workers’ compensation payments from other sources of income.

- Save any tax forms you receive, such as Forms W-2 or 1099 for unrelated income.

- Review any Social Security benefit statements if you receive SSDI.

- Report changes in your employment status when appropriate.

- Consult a qualified tax professional if your income comes from multiple sources.

Good organization throughout the year can make tax filing much easier.

When Should You Speak With a Tax Professional?

Many workers can file their taxes without difficulty because workers’ compensation benefits are generally tax-free.

However, professional advice may be helpful if you:

- Receive both workers’ compensation and SSDI.

- Receive pension or retirement income.

- Own a business or have self-employment income.

- Receive investment income.

- Have questions about a lump-sum settlement.

- Receive payments from multiple disability programs.

- Are unsure whether a payment is taxable.

A qualified tax professional can help you understand how federal tax rules apply to your individual circumstances.

Conclusion

So, is workers comp taxable? For most injured workers, the answer is no. Workers’ compensation benefits paid under a state’s workers’ compensation law for a job-related injury or illness are generally not subject to federal income tax.

However, your overall tax situation may become more complex if you receive additional income such as SSDI, retirement benefits, or investment income. While workers’ compensation itself usually remains tax-free, these other income sources may affect your tax obligations.

If you have questions about a workers’ compensation settlement, an SSDI offset, or multiple sources of disability income, reviewing the latest IRS guidance or speaking with a qualified tax professional can help you avoid costly mistakes.

Because tax laws and government programs can change, always verify the most current information through official government resources before making tax decisions.

Frequently Asked Questions (FAQ)

Is workers comp taxable by the IRS?

Generally, no. The IRS excludes most workers’ compensation benefits paid under a state’s workers’ compensation law from federal taxable income.

Do I need to report workers’ compensation on my tax return?

In most cases, no. Workers’ compensation benefits are generally not reported as taxable income on your federal income tax return.

Is a workers’ compensation settlement taxable?

Usually not. A lump-sum settlement that represents workers’ compensation benefits is generally tax-free. However, certain payments included in a settlement may have different tax treatment depending on the circumstances.

Can workers’ compensation affect SSDI?

Yes. Receiving workers’ compensation may reduce your SSDI benefits through a workers’ compensation offset if your combined disability benefits exceed the federal limit.

Will I receive a W-2 for workers’ compensation?

Generally, no. Workers’ compensation benefits are usually not reported on Form W-2 because they are not considered taxable wages.

Do I get a 1099 for workers’ compensation?

In most situations, no. Workers’ compensation benefits are generally not reported on Form 1099 because they are excluded from taxable income.

Is workers’ compensation considered earned income?

No. Workers’ compensation benefits are generally not treated as earned income for federal income tax purposes.